According to the Report on Trend and Progress of Banking in India 2024-25 of

RBI, the NPA of Indian banks has reached a multi-decade low, with the gross NPA ratio dropping to 2.1% by late 2025.

- The net NPA (NNPA) ratio also declined to 0.5 % at the end of March 2025

- GNPA ratio of banks started reached its peak in 2018 at 11.18%.

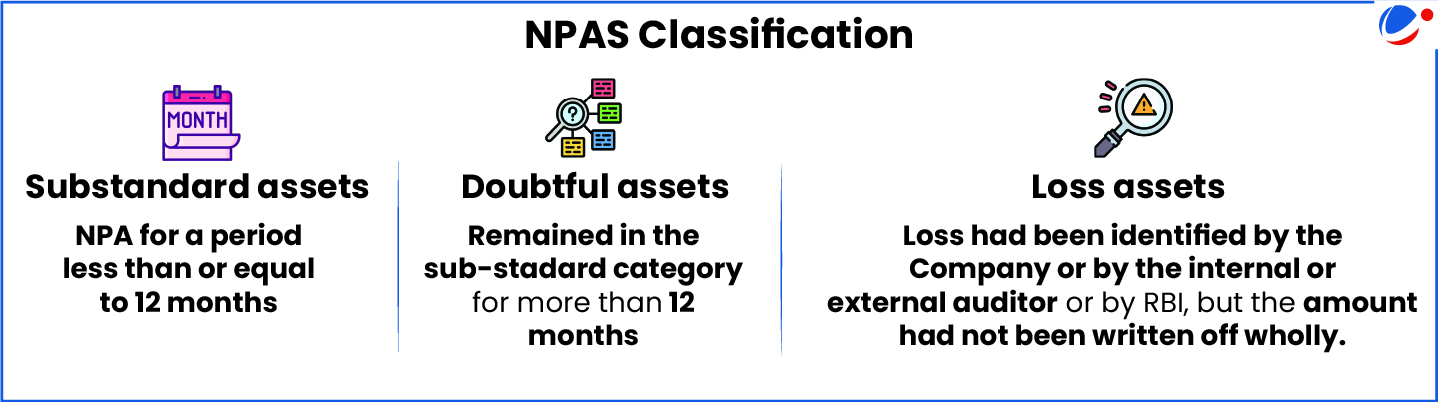

What is Non-Performing Assets (NPAs)?

- NPAs are loans or advances for which the principal or interest payment remains overdue for a period of more than 90 days.

- Gross NPA is the total value of loans where interest or principal remains overdue and Net NPA is obtained by subtracting provisions (the funds the bank sets aside to cover expected losses) from GNPA.

- Key Drivers of NPA: Economic slowdowns, fraudulent borrowers, poor monitoring, etc.

- Challenges associated with NPAs: high provisioning, reduced lending capacity, etc.

Key initiatives that have played a crucial role in reducing NPAs

- Insolvency and Bankruptcy Code (IBC), 2016: Created a time-bound and creditor-driven resolution framework for stressed assets

- Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 (SARFAESI Act): It allows secured creditors to take possession of collateral, against which a loan had been provided, upon a default in repayment.

- Asset Reconstruction Companies (ARCs): Banks continued to clean their balance sheets by selling NPAs to ARCs

- Other: Indradhanush plan (launched for revamping PSBs, envisaging infusion of capital in PSBs), Debt Recovery Tribunals (DRTs), etc.