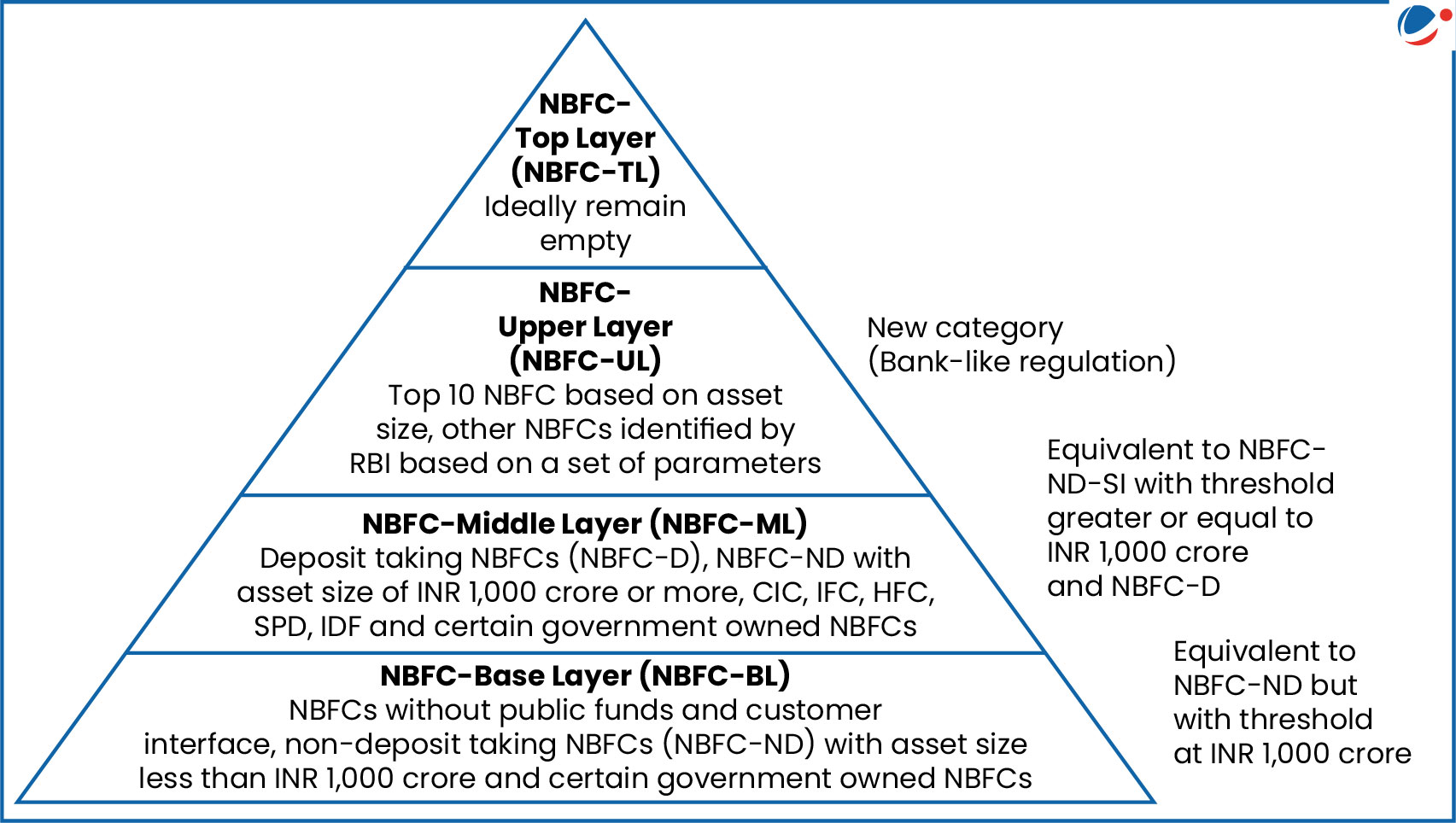

As per the current Scale Based Regulatory (SBR) framework, NBFCs are classified into four layers – Base, Middle, Upper and Top Layers (refer infographic).

Proposed amendments by the RBI

- New Criterion for Upper Layer NBFCs: A simple asset size of ₹1 lakh crore or more, replacing the current complex scoring model that identifies only top-ten NBFCs based on asset size.

- This threshold will be reviewed every five years.

- Inclusion of Government NBFCs: State-owned entities (like NABARD, Exim Bank, and SIDBI) will no longer be exempt and will face the same strict regulations as private NBFC-ULs.

- Unlimited State Guarantees: Upper-layer NBFCs to be permitted to use state government guarantees as a credit risk transfer mechanism without any quantitative caps.

What is a Non-Banking Financial Company (NBFC)?

- Definition: NBFC is a company registered under the Companies Act, 1956 or Companies Act, 2013, and engaged in the business of loans and advances, acquisition of shares, stocks, bonds, debentures, and securities.

- Regulation: primarily by the Reserve Bank of India (RBI), under Chapter III B of the Reserve Bank of India Act, 1934.

- However, some specific types of non-banking financial entities fall under the jurisdiction of other regulatory bodies to avoid overlap.

- For e.g. Insurance Companies - IRDA; Stock Broking & Merchant Banking – SEBI, etc.

Difference between Banks and NBFCs

|