The Standing Committee onFinance recently tabled an action taken report in the Parliament on observations and recommendations on the subject 'Performance Review and Regulation of Insurance Sector.

Key Observations by the Committee

Government policies on insurance: Imposition of 18% GST and Tax Deducted at Source acts as a deterrent to improving insurance penetration.

IRDAI has recommended exemption from taxation in line with developed countries like Canada and European Union.

Public Sector Insurance Companies: They face challenges of inadequate capital, lack of level playing field with private companies, overexposure to health insurance and lagging insolvency ratios (~₹ 26,000 crore financial losses).

E.g., Public Companies are mandated to deduct TDS on commissions, claims or bonuses paid to insurance agents and policyholders while private companies are exempted.

Increased private sector participation: The market share of private companies in the general and health insurance market increased from 48.03% in FY20 to 62.5% in FY23.

India allowed private companies in insurance sector in 2000, setting a limit on FDI to 26%, which was increased to 49% in 2014 and further increased to 74% in 2021.

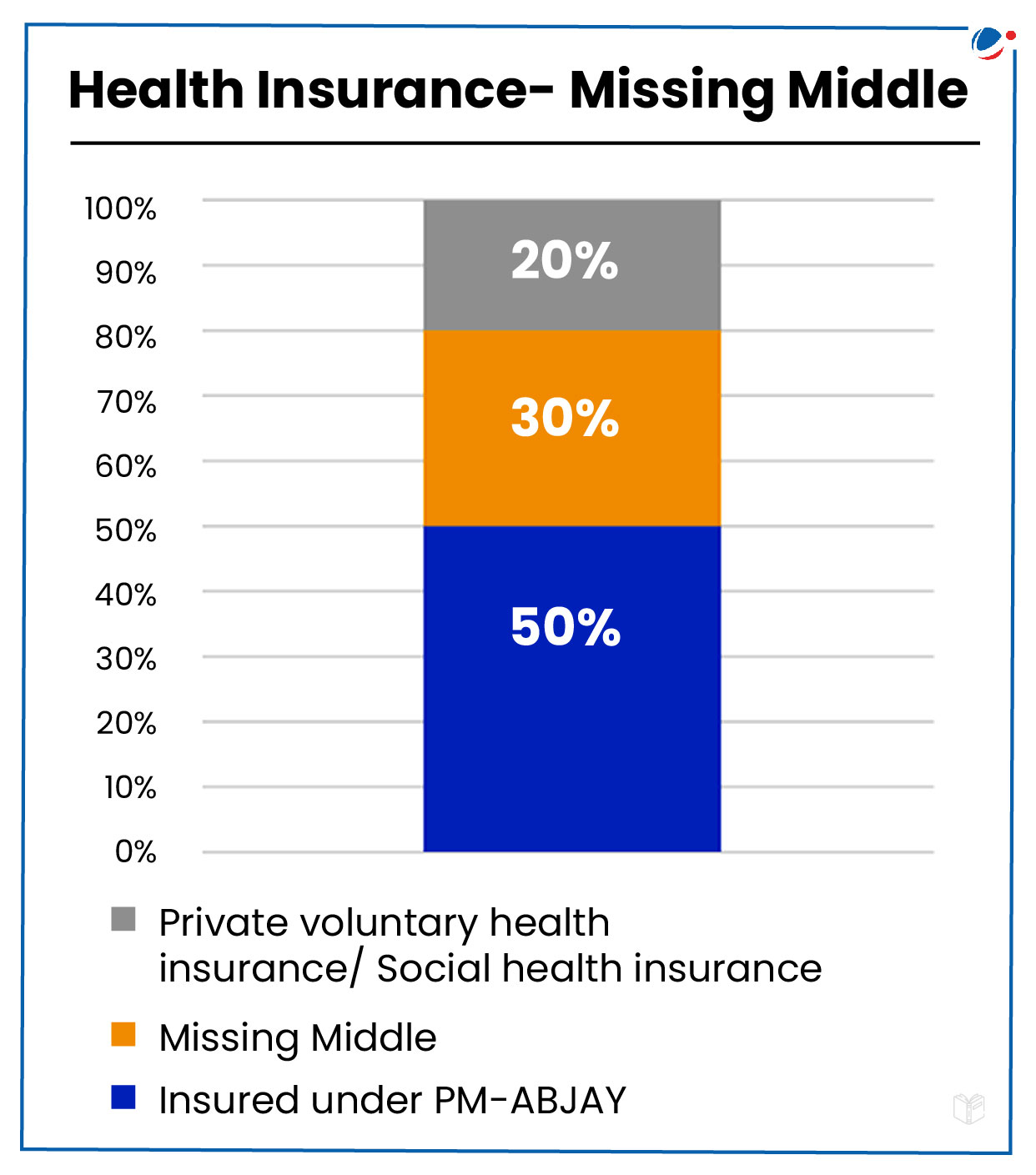

Missing Middle in Health Insurance: A significant portion of the population lacks adequate health insurance coverage. (See infographic)

Microinsurance: Challenges such as high transaction costs, lack of awareness, and the absence of a viable business model for intermediaries hinders growth of microinsurance.

Rising need for disaster coverage: India ranks 3rd, after the US and China, in the frequency of natural disasters since 1900 causing significant infrastructure and economic damage.

Repudiation/delay of large claims: Due to the competition, some private companies offer heavy discounts on premiums leading to inadequate fund for claim settlement. This leads to insurance companies deliberately avoiding claims settlement.

Micro-insurance

Micro insurance is specifically intended for the protection of low -income people, with affordable insurance products to help them cope with and recover from financial losses.

IRDAI (Micro Insurance) Regulations, 2015 define the eligibility criteria, product features, distribution channels, and reporting requirements for microinsurance.

As per Regulations, the sum assured under an Insurance product offering Life or pension or Health benefits shall not exceed Rs 200000.

Challenges: Small ticket size coupled with high transaction and service delivery costs, absence of a business model that can attract intermediaries, capacity building of intermediaries, and lack of basic awareness and knowledge on how insurance works.

Current micro-insurance products include PM Suraksha Bima Yojana, PM Jeevan Jyoti Bima Yojana, Pradhan Mantri Fasal Bima Yojana, Ayushman Bharat Pradhan Mantri Jan Arogya Yojana, etc.

Key Recommendations of the Committee

Promote Microinsurance: Developing new products and reducing the capital requirement for smaller insurance companies to promote financial inclusion.

It proposes to amend the Insurance Act, 1938, to remove the fixed capital requirement of Rs. 100 crore and enable IRDAI to set capital requirements through regulations.

Composite Licensing: Allow composite licensing for insurers to offer both life and non-life insurance products under one entity to reduce costs and improve customer choice.

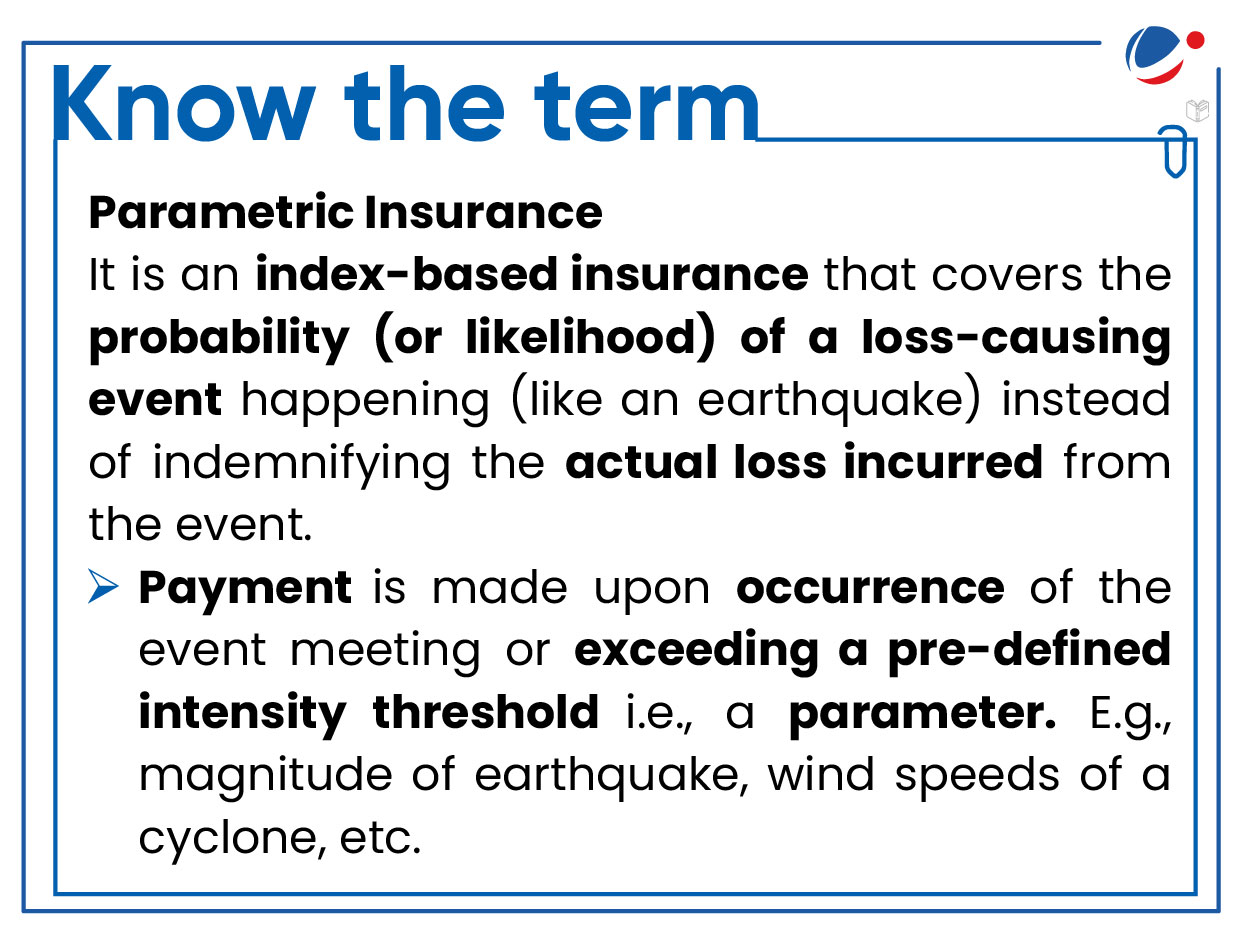

Parametric Insurance in disaster-prone areas: The government may provide insurance for homes and properties, particularly in vulnerable areas and among economically weaker sections.

E.g., incentivize insurance programme with subsidized premiums for disaster-prone areas like in Florida (USA)

Filling the Health Insurance gap: Constituting a multi-stakeholder Inter-Ministerial Working Group for long-term planning, developing simple and standardized products, sharing government data and infrastructure, ensuring the quality of services, and partial financing of health insurance should be initiated to increase health insurance coverage.

Reduce GST for health insurance and microinsurance products: GST rates applicable to health insurance products, particularly retail policies for senior citizens and microinsurance policies (up to limits prescribed under PMJAY, presently Rs. 5 lakh), and term policies may be reduced.

Level Playing Field for Public Sector Companies: Policy Roadmap White Paper be prepared with comprehensive stakeholder consultation for designing equitable insurance products.

Unclaimed Policies: Central Portal for unclaimed policies in line with UDGAM (Unclaimed Deposits: Gateway to Access information) of RBI to improve processing of a significant number of unclaimed policies that are currently being transferred to the Senior Citizen Fund.

Capital availability: The RBI on behalf of the Government may issue 'on-tap' bonds of various maturities up to 50 years as against the current maximum tenure of 40 years for investment by insurance companies.

The Insurance Regulatory and Development Authority India (IRDAI)

Statutory body under the Insurance Regulatory and Development Authority (IRDA) Act, 1999.

Objectives: Protecting the interests of the policyholders and regulating, promoting and ensuring orderly growth of the insurance industry in India.

The powers and functions of the Authority are laid down in the IRDA Act, 1999 and Insurance Act, 1938.

IRDAI is taking steps like Bima Sugam (e-marketplace platform), Bima Bharosa Grievance Redressal Portal, Bima Vahak (a women-centric dedicated distribution channel) and Bima Vistaar amongst other to fulfil its vision of 'Insurance for All by 2047'.